|

Phone: 877-216-7470 Email: Info@1stopcap.com Learn More |

Since: February 2024 Since: February 2024 |

Stories

Stop the Debt Settlement People, Funders Come Up With Merchant-Friendly Alternative

April 3, 2024 Are debt settlement “advisors” interfering with your contracts and putting your merchants in a bad spot? The industry is now taking the reins on a solution. It’s called GreenLedger, a platform for funders to work together on resolving a merchant’s situation with no debt settlement middlemen encouraging an intentional default, taking fees, and making false promises.

Are debt settlement “advisors” interfering with your contracts and putting your merchants in a bad spot? The industry is now taking the reins on a solution. It’s called GreenLedger, a platform for funders to work together on resolving a merchant’s situation with no debt settlement middlemen encouraging an intentional default, taking fees, and making false promises.

Founded by Elevate Funding CEO Heather Francis, who aims to eventually make it a non-profit, merchants would go to this industry-collaborative platform, indicate who they have open contracts with, and the platform would notify the funders directly.

“From there, the primary points of contact at each funder can get together to come up with a more specific and comprehensive payment plan that works with the merchant’s needs,” said Francis. “GreenLedger’s mission is to work directly with our small business clients to stabilize their revenue-based financing arrangements and avoid breaching their agreements, eliminating the need for potentially predatory middlemen.”

The platform has already been generating interest.

“As an attorney deeply committed to the financial empowerment of small and medium-sized businesses, I am thrilled to endorse Elevate Funding’s creation of GreenLedger,” said industry attorney Patrick Siegfried. “This initiative represents a pivotal step in our ongoing battle against the increasing prevalence of unscrupulous entities in the commercial finance debt settlement industry. Far too often, these bad actors employ deceptive sales tactics and bind clients with unfair contracts, leading not to the promised debt relief but to further financial strain for small businesses. GreenLedger, with its dedication to transparency and integrity, stands as a true avenue for business owners seeking legitimate and effective financial solutions. Its mission to root out malpractices and safeguard the interests of small businesses is not just commendable but essential in today’s challenging economic landscape.”

To learn how you can participate and cut the debt settlement people out of the picture, attend this webinar on April 16th.

Capify Announces New Appointment to Lead Broker Division

March 7, 2024Leading online SME lender, Capify, has appointed Mike Morris to lead its broker business in the UK.

Mike joins Capify after five years with Funding Circle, most recently as Head of Business Development, where he was responsible for leading the lender’s broker network.

With nearly 20 years experience in the finance industry, including time at Close Brothers retail finance, Mike will focus on the growth and expansion of Capify’s introducer relationships and its marketplace offering.

“I’m hugely excited to join Capify to build out its broker programme and exponentially grow this channel for one of the first online SME lenders in the UK market,” said Mike.

“Capify occupies a vital place in the funding landscape – offering much-needed fast, flexible and responsible solutions for businesses. We’re focused on ensuring that introducers understand our offering and how we can help their clients. Our growth will then be realised by launching new products that go up and down the credit spectrum, providing the best possible service to enable the brokers, and ultimately the clients they represent, to get the funds they need to thrive in the current climate. Our goal is to have an offering for all types of businesses so we can be a one-stop shop for brokers and their clients. I look forward to Capify announcing these new offerings in the near future.”

Capify was launched in the UK in 2008, against the backdrop of the global financial crisis, when many small and medium-sized businesses were struggling to access funding from banks. Last year it was named the UK Credit Awards SME Lender of the Year (up to £1m). The company was founded initially in the United States in 2002 making it one of the world’s first online alternative financing companies for SMEs globally.

John Rozenbroek, COO/CFO at Capify, said: “We’re absolutely delighted to welcome Mike to the Capify team. Brokers play an integral role in helping businesses understand the complex funding landscape and the types of finance that are best suited to their needs. His appointment underlines our commitment to introducers and marks an exciting new stage in Capify’s continued growth.”

ABOUT CAPIFY

Capify is an online lender that provides flexible financing solutions to SMEs seeking working capital to sustain or grow their business. Alongside its sister company, Capify Australia, the fintech businesses have been serving their respective markets for over 15 years. In that time, it has provided finance to thousands of businesses, ensuring the UK’s vibrant and vital SME community can meet the challenges of today and the opportunities of tomorrow.

For more details about Capify, visit: http://www.capify.co.uk

Capify Contact:

Ash Yazdani, Marketing Director

ayazdani@capify.co.uk

Media enquiries

Sam Gallagher, Director

sam.gallagher@1473media.com

Shopify Capital Renewal Rate Greater than 70%

February 13, 2024Shopify Capital’s funding business is continuing to gain momentum, according to the company’s latest quarterly earnings. Shopify stopped specifying precisely how much it is originating (perhaps because deBanked kept turning those numbers into posts every quarter for years) but still lists the receivables from its loans and merchant cash advances as a line item on its balance sheet. There the balance increased from $580M to $816 year-over-year.

“We know the capital product has been effective because we’re seeing a repeat renewal rate of over 70%, a testament to our ability to help merchants access the funding they need for growth, particularly ahead of key sale times, including the crucial Q4 holiday shopping season,” said Shopify President Harley Finkelstein during the call.

Originations Increased, Losses Decreased for Shopify Capital

November 2, 2023 Shopify Capital is still experiencing an increase in business loan and merchant cash advance originations, according to the company’s latest Q3 earnings report. The company recently stopped disclosing precisely how much it is they are originating, however. It used to give precise numbers but starting this year Shopify now only cites its loans and merchant cash advance receivables balance.

Shopify Capital is still experiencing an increase in business loan and merchant cash advance originations, according to the company’s latest Q3 earnings report. The company recently stopped disclosing precisely how much it is they are originating, however. It used to give precise numbers but starting this year Shopify now only cites its loans and merchant cash advance receivables balance.

“Transaction and loan losses decreased for the three months ended September 30, 2023 compared to the same period in 2022, primarily due to a decrease in losses related to Shopify Capital.”

So funding is up, losses are down, which is precisely the opposite situation that is going on at rival PayPal.

Shopify somewhat skimmed over its Shopify Capital business in its Q3 earnings announcements and on its official call except to state that it’s a strong segment that is growing.

Fintech Hasn’t Stopped. There’s Still Room for Constant Improvement in Lending

October 31, 2023 “I think fintech is a broad term,” said Frank McKenna, Chief Fraud Strategist at Point Predictive. “It can apply primarily to technology that enables faster banking, and more digital banking that hasn’t been satisfied with kind of the traditional brick and mortar banks or finance companies. Fintech can be banks, it can be platforms that provide the backbone for that kind of streamline lending. Or it can even be considered companies like ours, technology that helps financial companies make better decisions.”

“I think fintech is a broad term,” said Frank McKenna, Chief Fraud Strategist at Point Predictive. “It can apply primarily to technology that enables faster banking, and more digital banking that hasn’t been satisfied with kind of the traditional brick and mortar banks or finance companies. Fintech can be banks, it can be platforms that provide the backbone for that kind of streamline lending. Or it can even be considered companies like ours, technology that helps financial companies make better decisions.”

Fintech, which can take on any one of the forms McKenna described, has been causing transformations for over a decade and yet there are still processes in the lending world still ripe for improvement.

“[Fintech is] growing every day, it will be more because of timing,” said Richard Gusmano, CEO of BCCUSA. “I think we’re going to see more and more people doing it, especially with the SBA opening up lending to non-banks. You’re going to see more of it in many different fashions and derivatives and how they see it is going to continue to emerge.”

Gusmano’s company helps businesses secure bank lines and bank loans, a system that now includes its very own AI-powered solution. He’s already seeing how AI and machine learning technologies stand to disrupt processes in the small business finance ecosystem.

“There’s so many different ways to use it and it is not rocket science,” Gusmano said. “In the MCA space, it’s amount of deposits, it’s average daily balance, it’s business type, and other positions. AI can immediately pick up those things if programmed to do so. I would think that the MCA underwriters over time should be concerned because AI could likely do that and pick that up.”

But it’s not just about replacing manual processes, but also doing it in an efficient manner.

“Since most fintech is dealing in a non-face to face environment, you’re going to have a whole host of risk in fintech, more than you might have in a traditional bank,” said McKenna of Point Predictive, whose company collaborates with lenders to detect potential risks. “I can just name off five or six: you have higher rates of identity theft, use of fake IDs called synthetic identities, you have more falsified documentation, fake employers, people shot-gunning where they’ll go to multiple fintechs the same day and get as many loans as they can, as quick as they can. They call it shot gunning.”

McKenna added that if someone has no knowledge of how to navigate these types of strategies or does not have the right technology to handle it, they may fall victim to them.

The keyword there might be someone, as in a person

“The risks associated is that you still are going to need someone that can make human decisions, even with financial technology,” said Gusmano. “And if you don’t, you’re going to be keeping yourself away from businesses that you want to do business with. It can never be 100% tech.”

New California Disclosure Rules Reduce Capital Available to Small Businesses

March 21, 2023In a poll conducted by a leading trade association, since new CA disclosure rules were implemented in December 2022, 40% of respondents were found to be “no longer lending” to prospective borrowers who fall within the regulations’ threshold of less than $500,000. The poll was conducted by The Secured Finance Network (SFNet), an 80-year-old nonprofit with members representing the $4T U.S. secured finance industry. The new law, requiring sweeping financial disclosures, introduced by CA State Senator Steven M. Glazer in 2018, faced four years of strong opposition before being rolled out in December of 2022.

According to the poll, commercial finance companies would rather not lend to small businesses than comply with what they believe are “misguided and un-compliable” requirements. Mark Hafner, president and CEO of Celtic Capital Corporation, based in Calabasas, CA, said, “Unfortunately, we must now shy away from smaller deals (under the $500k threshold) as the disclosure requirements are extremely complicated to figure out and would require getting our attorneys and CPAs involved to ensure compliance. It’s just not worth the costs involved to fund a small deal anymore. The statute is not user friendly and, frankly, not representative of the true costs as there are numerous assumptions that have to be made to calculate the APR based on the state’s requirements. I honestly don’t think it was designed to meet the stated goal of the statute.”

Robert Meyers, president of Republic Business Credit, which does business with many California-based businesses, explained, “While the fines and penalties are clear under the regulations, the state has been unwilling to confirm our compliance or anyone else’s compliance. That fear is what has stopped 40% of our non-banks from doing business in the state, thus reducing access to capital for small- and medium-sized businesses. I expect this number to increase as time goes on. If the goal of this law was to better inform, it is actually doing the opposite as APR just doesn’t apply to our products.”

SFNet reports that its member companies provide “tens of billions” of capital annually in California to small businesses for essential working capital that funds everything from inventory, to work in process to payroll.

“Forty percent of billions is a large number,” said SFNet CEO, Richard D. Gumbrecht. “In attempting to find a one-size-fits-all solution to financial transparency, the State has created a complex set of requirements that misrepresent the actual cost of borrowing. Lenders are saying it’s not worth the cost and risk of complying. If this sample of 50 lenders is indicative of what we can expect, clearly that was not the intent of the legislation. And considering the demise of Silicon Valley Bank, it’s more important than ever that capital is not restricted in California.” The trade association is working with State legislatures to revise the statute. “Other states have found a simpler and more accurate way to protect small borrowers, and given the unintended consequences we are seeing, we are hopeful California will be receptive to these alternative approaches.”

To demonstrate how vital small businesses are to the U.S. economy, and the importance of not curtailing funding, consider these statistics: According to the U.S. Small Business Association (SBA), small businesses of 500 employees or fewer make up 99.9% of all U.S. businesses and 99.7% of firms with paid employees. Of the new jobs created between 1995 and 2020, small businesses accounted for 62%—12.7 million compared to 7.9 million by large enterprises. A 2019 SBA report found that small businesses accounted for 44% of U.S. economic activity.

About Secured Finance Network

Founded in 1944, the Secured Finance Network (formerly Commercial Finance Association) is an international trade association connecting the interests of companies and professionals who deliver and enable secured financing to businesses. With more than 1,000 member organizations throughout the U.S., Europe, Canada and around the world, SFNet brings together the people, data, knowledge, tools and insights that put capital to work. For more information, please visit SFNet.com.

Media Contact:

Michele Ocejo, Director of Communications

Secured Finance Network

mocejo@sfnet.com, 551-999-5283

NYC’s Small Business Loan Program Stops Accepting Applications After Just 3 Weeks

February 13, 2023 The opening of NYC’s $75M Small Business Opportunity Fund backed by a combined partnership of Goldman Sachs, Mastercard, Community Reinvestment Fund, and CDFIs was heralded as historic. Cheered as the largest public-private loan fund ever directed at small businesses, which stood to offer 5-6 year loans up to $250,000 at a rate of 4% interest to help them recover from the pandemic, the program kicked off on January 23. Just three weeks later, however, the acceptance of new applications has been halted.

The opening of NYC’s $75M Small Business Opportunity Fund backed by a combined partnership of Goldman Sachs, Mastercard, Community Reinvestment Fund, and CDFIs was heralded as historic. Cheered as the largest public-private loan fund ever directed at small businesses, which stood to offer 5-6 year loans up to $250,000 at a rate of 4% interest to help them recover from the pandemic, the program kicked off on January 23. Just three weeks later, however, the acceptance of new applications has been halted.

“Due to the high level of interest, the NYC Small Business Opportunity Fund has temporarily paused intake of new applications while our lending partners assess completed applications,” the official website states. News reports claim the that fund was swarmed with 10,000 applications.

Indeed, that is already more than 6x the maximum number of loans that the fund was set up to support. The Fund envisioned a maximum of 1,500 total loans originated before the capital was exhausted. The approval criteria itself is lenient as the fund boasts that there is no minimum credit score requirement. Documentation supporting an ability to repay the loan is required, however.

Businesses that didn’t apply early are told that they can fill out an inquiry form to be notified if the fund reopens.

Deal Gone Bad? Next Stop Arbitration

June 20, 2022 When a funder is unable to resolve a breach of contract with a customer on its own, litigation may seem like the only option left. But there may be an alternative, a process known as arbitration.

When a funder is unable to resolve a breach of contract with a customer on its own, litigation may seem like the only option left. But there may be an alternative, a process known as arbitration.

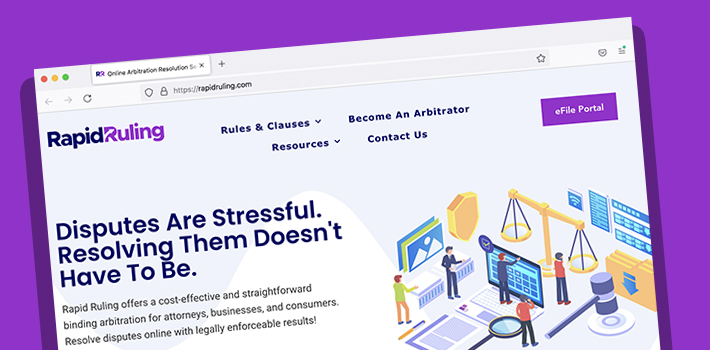

“Arbitration is a creature of contract,” said Zachary Meyer, a partner at a law firm. Meyer is also the co-founder and Chief Administrator of RapidRuling, an arbitration forum that has recently experienced an uptick in cases from the small business finance space. An arbitration forum is an alternative to the courthouse, where disputes are adjudicated by an arbitrator instead of a judge. It’s binding. The prevailing party, for example, can take an arbitrator’s award to the Court and turn it into a judgment.

Meyer told deBanked that part of the original vision for RapidRuling was an entirely online system that would prevent one or both parties from having to incur travel costs to participate. The overall cost of arbitration for a respondent in Montana, for example, would go up if they had to pay for a flight to New York City just to appear for it. “It’s beneficial for the [respondent],” Meyer said.

But in 2019 when RapidRuling first launched, the industry was already well accustomed to relying on AAA, the acronym for the American Arbitration Association. AAA, which was founded in 1926, resolved more than 300,000 total cases in 2019 alone. But then, Covid hit.

“It was like a perfect storm,” Meyer said. As the court system ground to a halt and struggled to move online, an all-online arbitration forum like RapidRuling suddenly had significant appeal. Meyer explained that the forum’s low filing fee compared to alternatives also grabbed attention. It understandably took off.

But the path to arbitration, including which forum to rely upon, may all hinge on the original contract itself, which a funding company’s attorney should carefully draft. Copying and pasting a random contract off the internet, for example, carries great risk, Meyer explained, because one may later discover a boilerplate arbitration clause to be limiting or disadvantageous.

RapidRuling’s website describes its arbitration process in four steps:

1. Submit Your Dispute

2. Wait For Opposing Party To Respond

3. Arbitrator Reviews Submissions

4. Receive An Arbitration Award

Contrast that value proposition to litigation, which depending on the circumstances could be drawn out for years.

RapidRuling seeks out arbitrators that are well-qualified, fair-minded, and diverse. “We have a panel of six arbitrators right now,” Meyer said, “and we’re looking to add more.”